The Lynx Case: How the AFM Read Article 44(2)(c) and What It Means for MiFID II Firms

In April 2025, the Dutch Authority for the Financial Markets (AFM) fined Lynx B.V. €300,000 over the way its advertising presented risk warnings. Lynx lodged a formal objection. In October 2025 the AFM rejected that objection, with supplemented reasoning, and Lynx chose not to take the matter to court. The fine is final.

The formal finding was about presentation rather than misleading product content. The case was not framed as a suitability case or a hidden-fees case. It centred on the presentation of risk information under Article 44(2)(c),the rule on how a required risk indication must be set out. A risk indication did exist in several of the advertisements, in the base creative or on the page, but that was not the end of the matter. In some of the Google Demand Gen and responsive-video formats the warning could become unreadable, and some of the headline and description combinations Lynx supplied carried no risk indication at all. What mattered to the AFM was whether the warning actually did its job once the advertisement reached a reader, not simply whether one could be found somewhere in the material.

The case is worth examining in detail, because it shows how regulators apply Article 44 of the MiFID II Delegated Regulation in practice, and what the gap between having a disclosure and having a compliant one actually looks like.

Related CPD seminar. This Lynx case features in Marketing Communications, Gamification and Digital Engagement under MiFID II, our CPD course on marketing communications, risk-warning prominence and digital engagement. The course includes practical tools, including a Lynx-style risk-warning prominence test for compliance and marketing teams. View the course.

What Article 44(2)(c) Requires

Article 44 of Commission Delegated Regulation (EU) 2017/565 applies to information, including marketing communications, that investment firms address to retail or professional clients, or to potential retail or professional clients, as well as information distributed in such a way that it is likely to be received by those clients. The principle behind it is simple enough.

When a firm draws attention to the potential benefits of a service or financial instrument, it must also give an accurate and clear indication of the relevant risks. Article 44(2)(c) then sets specific requirements for how that risk indication is presented. It must use a font size at least equal to the predominant font size used throughout the information, and a layout that ensures the risk indication is prominent.

The AFM's position, confirmed in this case, is that the test is not whether the risk warning is technically present, but whether a real consumer, looking at a real advertisement, can take the warning in and weigh it before deciding. The font size and layout requirements are there to prevent disclosures that are formally included but easy to miss in practice.

The Campaign and the Violations

The advertising at issue came from a welcome offer: new clients could receive up to €500 of their transaction costs back when they opened an account. The AFM examined this campaign over the period from 1 December 2023 to 1 March 2024. The advertisements it selected had been published between 1 December 2023 and 24 February 2024, while the firm's homepage was captured separately on 19 March 2024. The offer appeared across print magazines, news websites, Google display and video advertising, and the Lynx homepage.

Scale is part of the story, and so is the AFM's restraint about it. Over the reviewed period, from 1 December 2023 to 1 March 2024, Lynx had published more than 2,500 advertising expressions across 23 channels. The AFM did not allege that all of them breached the rules. It selected five expressions, together with the homepage, and found a violation in each. The case is therefore not mainly about volume. It is about a presentational imbalance the regulator was prepared to act on where the risk indication was not prominent enough in practice.

The defects fell into two broad categories, font size and layout. In most of the selected expressions the risk warning was the smallest, or close to the smallest, text on the page. In several, the layout made the warning hard or impossible to notice even where the font size itself might have passed.

The advertisements below show several of the Lynx expressions the AFM examined.

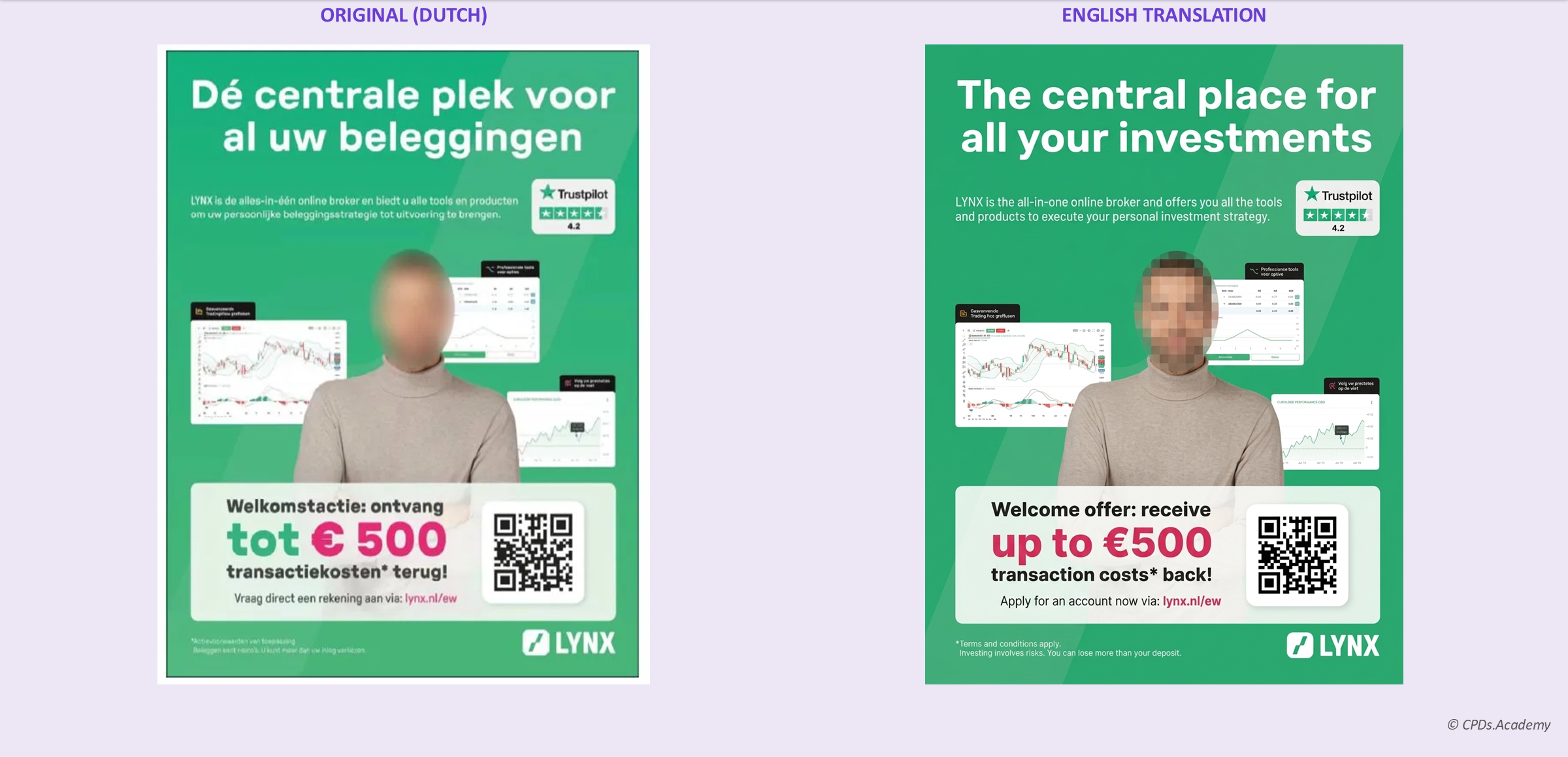

Advertisement 1 — Print magazines (EW, 11 January 2024, and Beleggers Belangen, 18 January 2024)

Caption: The two magazine advertisements were identical apart from the URL and QR code. A page-sized green advertisement is dominated by the headline "The central place for all your investments" and the welcome offer, with the €500 figure in bold pink and a large QR code. The risk warning sits in the bottom-left corner in small white text on the green background. The AFM found the font size too small and the white-on-green contrast insufficient, a breach on both the font size and the layout limb of Article 44(2)(c).

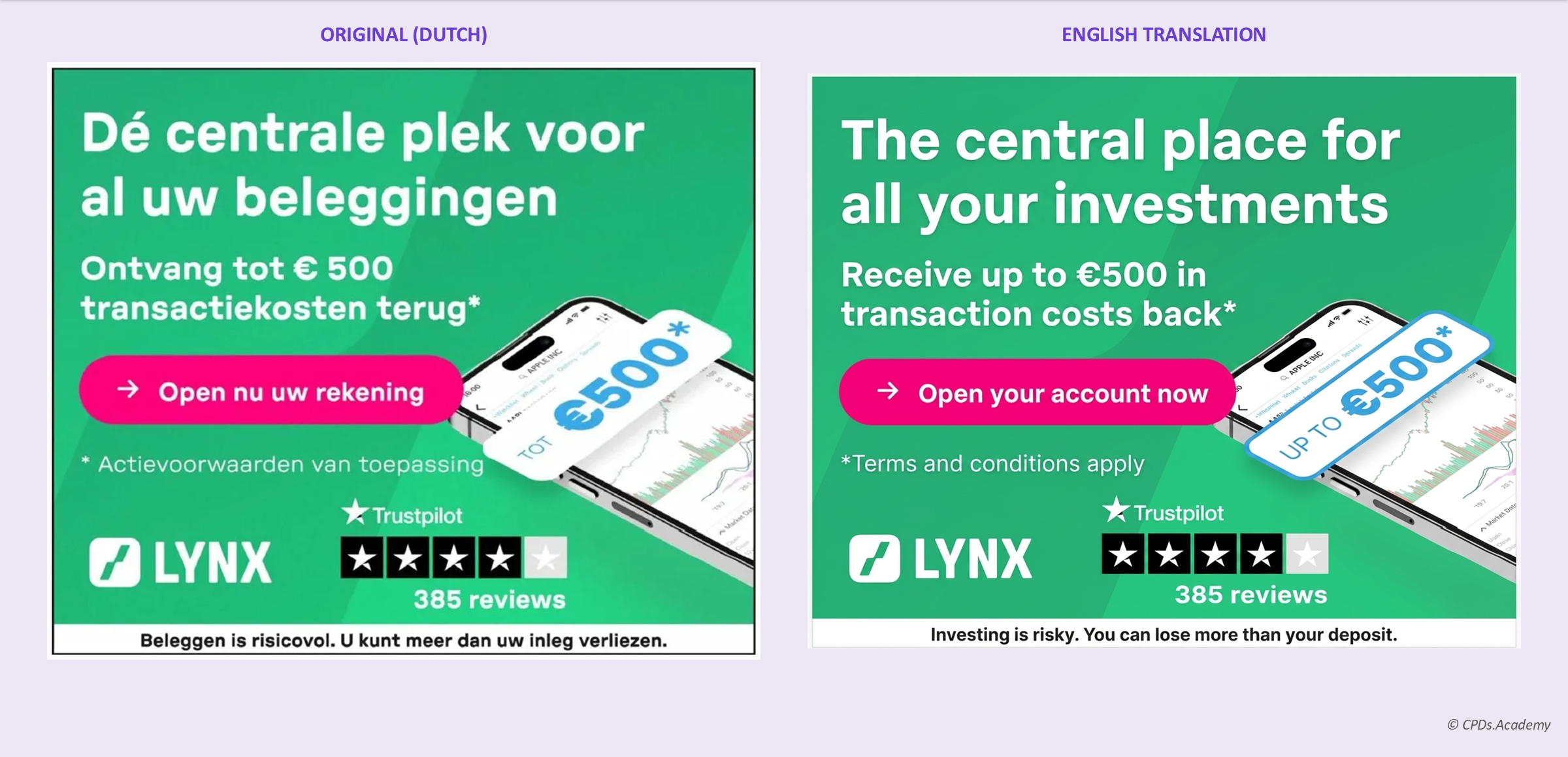

Advertisement 3 — Telegraaf.nl banner (15 January to 9 February 2024)

Caption: A near-square green banner. The offer, the rating and the call to action all appear in large, prominent type. The risk warning "Beleggen is risicovol. U kunt meer dan uw inleg verliezen." ("Investing is risky. You can lose more than your deposit.") is present, but it is the smallest text on the advertisement. Here the AFM's finding was about font size alone: the risk warning was clearly smaller than the predominant font size used elsewhere in the advertisement.

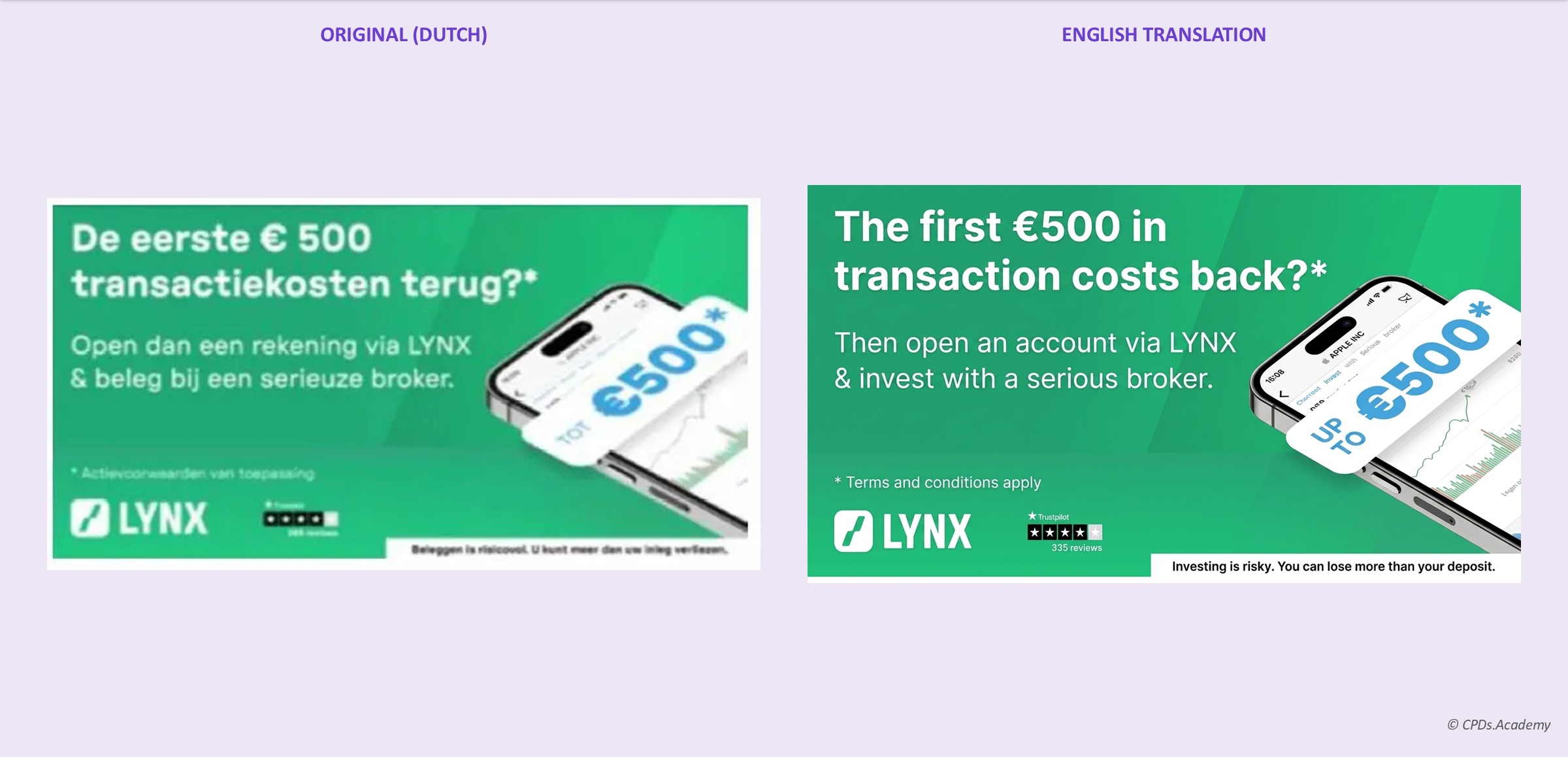

The same imbalance recurred across the other expressions the AFM examined, though the precise defect changed with the format. On the iex.nl banner, the risk indication was in the visually smallest font and was also placed in a way that made it easy to overlook. The issue there was not low contrast in the ordinary sense: the warning was black text on a white strip. The problem was that the strip sat over a white phone image and was visually overtaken by larger, brighter elements. On the homepage, the first risk indication failed on layout rather than font size, boxed away and reachable only far down the page. What stayed constant was the visual hierarchy: the offer drew attention first, while the risk warning sat at the margins.

Two further expressions are worth looking at separately, because they show a dimension of the problem that goes beyond font size.

Advertisement 4 — Google Demand Gen image ad (1 December 2023 to 24 February 2024)

Caption: The Demand Gen creative shown here was served across YouTube, Google Discover, Gmail and the Google Display Network, resized to suit each format and device. The headline and the broker-confidence claim dominate, while the risk warning, "Beleggen is risicovol. U kunt meer dan uw inleg verliezen." ("Investing is risky. You can lose more than your deposit."),sits in a thin strip along the very bottom. The AFM found that when the image was served small, for example as a Gmail thumbnail, that bottom-strip warning became unreadable, and that some of the headline-and-description combinations Lynx supplied carried no risk indication at all, so in those rendered formats there could be no readable risk warning in the advertisement as a whole.

The AFM's reasoning here matters. Lynx was responsible for how its advertisements were configured across every display format. Where a campaign set-up lets the risk warning disappear depending on how the advertisement happens to be rendered, that is not an acceptable outcome. The obligation to make the warning prominent applies in every format.

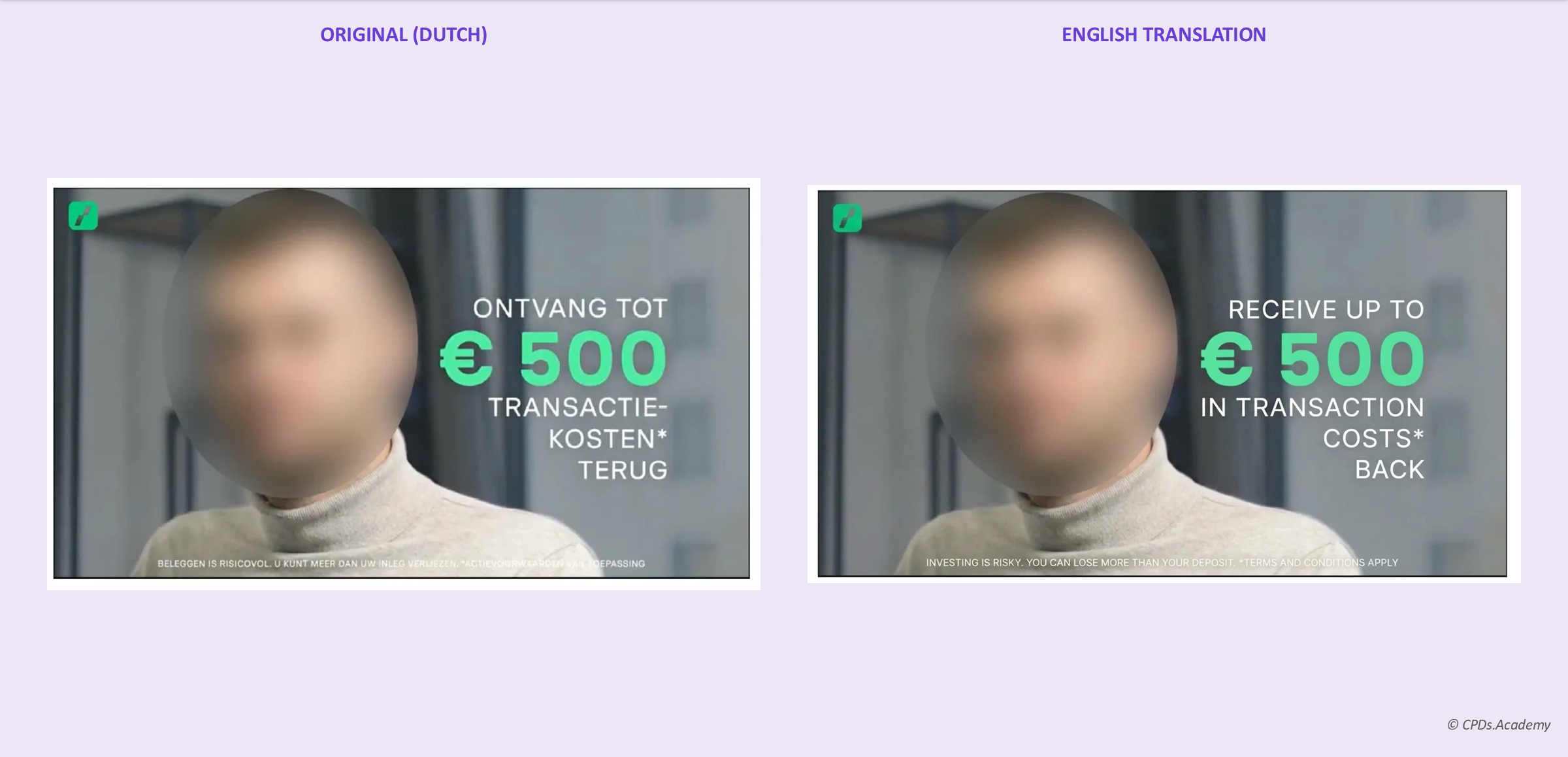

Advertisement 5 — Google Responsive Video Ad (29 January to 11 February 2024)

Caption: A still from the 15-second video advertisement, which had no spoken words. The risk warning "BELEGGEN IS RISICOVOL. U KUNT MEER DAN UW INLEG VERLIEZEN." appears in small white text at the bottom of the frame. For parts of the video the text sits against a pale background, a beige sweater or a white desk, so the contrast falls away and the warning becomes very hard to read. The AFM found that, because of the moving images, the risk warning was not clearly readable during the first eight seconds, a layout failure under Article 44(2)(c).

The homepage showed the same pattern at full length. When the AFM captured it on 19 March 2024, the part visible on opening, above the fold, sold the service and carried no risk indication at all. The risk indications did exist, but only well down a long page.

Caption: The second risk warning on the Lynx homepage, in a narrow white strip at the very bottom of the sixth and final screen: "Let op: beleggen brengt risico's met zich mee. Uw totale verlies kan aanzienlijk hoger zijn dan uw totale inleg." ("Please note: investing carries risks. Your total loss can be considerably higher than your total deposit."). It was the smallest font used anywhere on the homepage, wedged between a white content block and the black footer. The AFM noted that the footer's own white text stood out more sharply than the risk warning did.

The first of the two homepage risk indications sat near the bottom of the fourth screen of six, inside a grey box and partly hidden behind a "read more" control, so the full text appeared only after the reader actively expanded the section. The AFM found that the grey box did not invite reading, and that the portion left visible was too general to do the work of a risk indication.

The Firm's Prior History and the Fine Calculation

What turned this into a financial penalty rather than another informal correction was the supervisory history. Between 2013 and 2021 the AFM had taken Lynx to task over its advertising six times, escalating from a norm-conveying letter in March 2013 to a formal warning letter in December 2021. The AFM described a recurring pattern, in which Lynx would act once the regulator identified a problem, only for similar shortcomings to reappear later.

Lynx argued that this history should carry little weight, on the basis that the earlier interventions had concerned the benefit-and-risk balance under Article 44(2)(b) rather than the font-and-layout requirement under 44(2)(c). The AFM did not accept that. It treated the two limbs as closely connected, and noted that Lynx had already been pointed to the text and the operation of Article 44(2)(c). The earlier conduct therefore counted against the firm. The AFM stopped short of raising the penalty for culpability, but only because it had already weighed the supervisory history when it decided to impose a fine at all.

The decision also observes that Lynx ran a full-scale advertising operation with close attention to design and layout, which made it harder to accept that the placement and contrast of its risk warnings were simply accidental oversights.

The fine itself was calculated in steps. The statutory base amount for this category of violation was €500,000. The AFM made no upward adjustment for the seriousness or duration of the breach, and none for culpability. As noted above, the repeat conduct would ordinarily have justified a culpability increase, but the AFM had already taken the supervisory history into account when deciding to impose a fine at all, so a further increase would have gone too far. The amount was then reduced to €300,000 at the proportionality stage, for two reasons. The proven breaches involved a limited number of expressions within a general promotional campaign, and Lynx had cooperated openly during the investigation and taken concrete remedial steps after the April 2024 warning conversation. Under an external project manager, it reviewed and improved its entire client-information process, including the controls across its three lines of defence, and ran additional training for its marketing teams. After its objection was rejected, Lynx did not take the decision to court, and the fine became final.

What This Means in Practice

Article 44(2)(c) applies across the EU, and it binds investment firms regulated by CySEC just as it bound Lynx. The AFM decision is not binding on other national competent authorities, but it is a useful reference point for how the presentation rule may be read in practice.

For compliance and marketing teams, the practical question is not whether a risk disclosure appears somewhere in a communication, but whether it works. That turns on whether its font is genuinely comparable to the surrounding text, whether it has enough contrast to be read, whether its placement means a real reader will actually encounter it, and whether it holds up across every format and screen size in which the communication is served.

The AFM made one further point worth carrying forward. Firms put real care into the visual design of their advertising, and their font choices, colour palettes and layouts are deliberate. The regulator reads the presentation of risk warnings through that same lens. On this reasoning, a warning that meets a bare technical threshold while sitting visually beneath every other element on the page is not an effective disclosure, however accurate its words.

That is the standard the AFM applied here.

Sources: AFM penalty decision (boetebesluit) concerning Lynx B.V. of 17 April 2025, the AFM decision on objection of 15 October 2025, the AFM case-status update, and Article 44(2)(c) of Commission Delegated Regulation (EU) 2017/565.

Turn this into competence your team can evidence. Our CPD seminar Marketing Communications, Gamification and Digital Engagement under MiFID II uses the Lynx case and other enforcement examples to help compliance and marketing teams test whether risk warnings are prominent in practice. View the course.

Article by Nikolas Demetriades

Published 04 Jun 2026